How to Track Cash Advances in a Company

Learn how finance teams track, control, and reconcile cash advances with approval workflows, UPI-native payouts, and real-time audit trails using CUPI

How to Track Cash Advances in a Company (A Finance Team's Practical Guide)

TL;DR

A cash advance is company money given to an employee before a business expense occurs — unlike reimbursements, which happen after.

Most companies lose track of advances because there's no structured approval, no spend limit, and no automated reconciliation — just trust and follow-up emails.

The right tracking system creates a four-step chain: request → approval → controlled payout → reconciliation. With CUPI, UPI rails compress this into near real-time — eliminating the manual request-and-wait bottleneck entirely.

With CUPI, the employee operates as an authorized user within the company's corporate account — spend-capped and purpose-locked — not as an independent recipient of a personal payout.

Cash advances without controls create three specific risks: float abuse (money sits with employees too long), category drift (spends go outside approved purpose), and duplicate or inflated claims.

Key controls finance heads should require: per-advance spend caps, purpose tagging, receipt mandates, and a hard settlement deadline.

A structured system doesn't just prevent fraud — it cuts month-end close time because reconciliation is already done by the time you need it.

In most Indian companies, cash advances still work like this: an employee asks a manager, the manager says yes verbally, someone hands over cash or does a quick IMPS transfer, the employee spends it, and then — weeks later — a crumpled receipt lands in someone's inbox. The reconciliation follows. Sometimes.

That gap between "money out" and "money accounted for" is where leakage lives. This guide explains how to close it.

What Is a Cash Advance — and Why Is It Hard to Track?

A cash advance is money your company gives an employee ahead of an expense. The employee spends it, then accounts for it. This is different from a reimbursement (where the employee pays first, claims later) and different from a corporate card (where the company pays a bank bill after the fact).

Cash advances show up across most operations-heavy Indian businesses:

A sales rep travelling to a Tier-2 city for a client visit

A field executive who needs to pay a local contractor in cash

A procurement officer picking up supplies from a vendor who doesn't accept NEFT/cards

A logistics coordinator managing last-mile expenses across multiple routes

The reason tracking breaks down is structural. Most businesses issue advances informally — a message, a transfer, and a reminder to "submit bills by Friday." There's no system enforcing that. The result is open float (advances that haven't been settled), no audit trail, and reconciliation that depends on people chasing people.

Why Does This Matter to Finance Teams Right Now?

According to the RBI's Payment Systems Report, UPI accounted for 85.5% of digital payment transaction volume in H2 2025 — yet most internal employee payout workflows haven't caught up. Companies run UPI for everything external, but internally, cash advances still flow through informal bank transfers with zero controls attached.

UPI recorded 228.3 billion transactions in 2025, up from 172.2 billion in 2024 — a 29.3% volume increase. Every operations-heavy company is touching UPI daily. The infrastructure exists. The controls layer on top of it often doesn't.

The practical consequence: finance teams spend time they don't have chasing settlement on money they've already sent out.

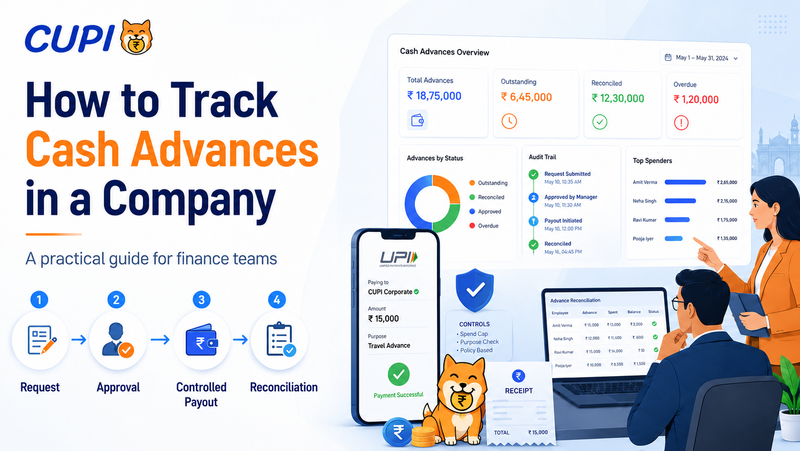

How Does a Cash Advance Tracking System Work? (Step-by-Step)

A structured cash advance workflow has four stages. Here's what each one should look like in practice.

Step 1 — Request

In a traditional system, the employee submits a request specifying:

Amount needed

Purpose (travel, procurement, field ops, etc.)

Date of expense

Expected settlement date

This creates a paper trail from moment zero — no more verbal approvals. But this step is also where most processes stall. Requests wait in inboxes. Approvals lag. Employees follow up. Money eventually moves, but the expense has often already happened by then.

With CUPI, this bottleneck doesn't exist. Because CUPI operates on UPI rails, spend data is captured at the point of transaction in near real-time — against a pre-configured corporate account. The company's guardrails (spend caps, purpose categories, MCC restrictions) are already set at the account level. There's no slow request-and-wait cycle before an employee can operate. The controls travel with the account, not the approval email.

Step 2 — Approval

A configurable approval chain reviews and approves (or rejects) the request. In CUPI, this is multi-level — a team lead approves, then a finance manager, depending on the amount bracket. Approvals happen on mobile, so the process doesn't wait for someone to be at a desk.

Critical controls at this stage:

Spend cap enforcement (you set ₹5,000 max for this category; the system won't let you approve ₹12,000 without an override)

Purpose-category locking (a "travel" advance can't be used for procurement)

Validity window (the advance is active for 3 days; unused amounts auto-expire)

Step 3 — Controlled Payout

Once approved, the advance is activated within the company's corporate account on UPI rails. The employee isn't receiving a personal payout into their own account — they're operating as an authorized user within the company's account, with a pre-defined spend envelope attached to their role or trip.

The company remains the account holder throughout. The employee operates within guardrails set by finance: spend cap, purpose category, MCC restrictions, and validity window. They can transact at any UPI QR — kirana, fuel pump, logistics vendor — without needing a card or physical cash. But every rupee spent is debited from the corporate account, not a personal float.

Every transaction is logged in real time against the advance ID.

Step 4 — Reconciliation

After the expense window closes, the employee submits receipts. CUPI matches spend data (already captured from the UPI transaction) against submitted bills. Unmatched or over-limit spends flag automatically. Settled amounts close the advance; unspent amounts are flagged for return.

Finance doesn't chase anyone. The data is already there.

What Controls Do Finance Teams Actually Need?

Most finance heads don't need more data — they need fewer exceptions. These are the controls that eliminate the common failure points:

Per-Advance Spend Caps

Every advance should have a hard ceiling. ₹2,000 for local field ops. ₹15,000 for outstation travel. The system enforces these — it doesn't just recommend them.

Purpose Tagging

An advance issued for "client visit — Chennai" should not be reconcilable against grocery receipts. Purpose tagging lets finance categorise spend at issuance and flag deviations at reconciliation.

Settlement Deadlines with Auto-Escalation

The advance closes on Day 5. If the employee hasn't submitted receipts, the system escalates — first a reminder, then an alert to their manager. No manual follow-up required.

Merchant Category Restrictions (MCCs)

For companies using CUPI's UPI payout layer, you can restrict which merchant categories an advance can be used at. A logistics advance can include fuel (MCC: 5541) and toll (MCC: 7523). It cannot include restaurant charges (MCC: 5812) unless approved separately.

Immutable Audit Trail

Every action — request, approval, payout, spend, receipt upload, settlement — is timestamped and stored. This is what your auditor needs. This is what prevents disputes.

Configurable Approval Chains

Not every advance needs the CFO's sign-off. A ₹1,500 petty cash advance should clear in one step. A ₹50,000 vendor payment advance might need three. Configure by amount bracket, not by individual exception.

Real Use Cases: How Companies Track Advances in Practice

Use Case 1 — Field Sales Team (50+ reps, Tier-2/3 cities)

A FMCG distributor has 60 sales reps operating across Karnataka and Tamil Nadu. Previously, advances were issued via informal IMPS transfers. Settlement was weekly — except when it wasn't. With CUPI, each rep is set up as an authorized user within the company's corporate account, with a trip-scoped spend limit pre-configured by finance. Spend is captured automatically at point of transaction. Finance reconciles 60 accounts in an afternoon instead of three days.

Use Case 2 — Procurement Ops (Local Vendor Payments)

A manufacturing SME needs to pay local raw material suppliers who don't accept NEFT but do accept UPI QR. The procurement officer gets a purpose-locked advance of ₹40,000 for approved vendor categories. Every payment scans directly at the vendor's QR. Receipt and transaction data are already matched by the time the bill is submitted.

Use Case 3 — Event / Marketing Ops

A marketing team running a product launch needs ₹1.2L in operational cash — venue deposits, logistics, F&B for a 2-day event. Instead of one large transfer with zero visibility, CUPI issues category-split advances: ₹40k venue, ₹30k logistics, ₹25k catering, ₹25k contingency. Each category reconciles separately. Post-event close takes 2 hours, not 2 weeks.

Use Case 4 — Site Ops / Construction

A mid-size construction company runs 12 active sites. Each site supervisor needs daily petty cash for materials, labour, and sundries. CUPI issues daily rolling advances with auto-reset. Supervisors spend via UPI. Finance gets a consolidated site-wise spend dashboard in real time.

Use Case 5 — Logistics / Fleet Management

A logistics company with 200 drivers issues per-trip advances for fuel, toll, and maintenance. With MCC restrictions, fuel-only advances can't be used at restaurants. GPS tagging on select spends confirms location at point of spend. Month-end close is pre-reconciled.

Use Case 6 — RevOps / Client Onboarding Costs

A SaaS company's customer success team incurs onboarding-related costs — travel, software subscriptions, small vendor payments. These used to flow through personal cards and reimbursement claims. With structured advances, CSM spend is tagged to the client account from day one. Finance and RevOps have shared visibility into cost-per-account.

Comparison Table: CUPI vs Cash vs Reimbursements vs Cards vs Bank Transfers

Conclusion

Tracking cash advances isn't a complex problem. It's a process problem — the work is done manually because most companies never built the system to do it automatically.

The switch to structured advance management doesn't require a large implementation. It requires four things: a request step, an approval chain, a controlled payout, and a reconciliation close. A modern system handles all four without the delays that make the traditional process frustrating.

If your finance team is still chasing settlement emails at month-end, that's the clearest sign the current process isn't scaling.

CUPI is a B2B payments control platform built for exactly this. It lets finance teams issue UPI-native payouts to employees — as authorized users within the company's corporate account — with pre-set spend limits, multi-level approvals, MCC-level restrictions, and automatic reconciliation on UPI rails. Purpose-built for Indian businesses that need controls, not just transfers.