# About

Name: CUPI

Description: CUPI makes business payments simple. Pay vendors, manage petty cash, clear office bills, handle travel spends, and track reimbursements without the usual confusion. Your team can pay easily, and your finance team can see where the money is going. Read our blogs to learn how businesses can stop small cash leaks and manage expenses better with CUPI.

URL: https://blog.getcupi.com

# Navigation Menu

- Visit Website: https://www.getcupi.com/

- Check your cash leakage: https://www.getcupi.com/calculator

# Blog Posts

## Cash Advance Management for Field Employees : What Actually Works in India

Author: Nithish B

Author URL: https://blog.getcupi.com/author/nithish-b

Published: 2026-06-10

Category: Writing

Category URL: https://blog.getcupi.com/category/writing

Meta Title: Cash Advance Management for Field Employees | CUPI

Meta Description: Finance teams lose control the moment cash leaves the office. See how CUPI replaces petty cash advances with UPI-native payouts, approval workflows, and real-time reconciliation.

URL: https://blog.getcupi.com/cash-advance-management-field-employees

## Finance teams lose control the moment cash leaves the office. See how CUPI replaces petty cash advances with UPI-native payouts, approval workflows, and real-time reconciliation.

**CUPI** (by EscrowStack) is a controlled payout platform that lets finance teams issue, approve, track, and reconcile cash advances to field employees entirely over UPI, without handling physical cash or waiting for receipts at month-end.

If your field team runs on cash advances today, this is for you.

Replacing physical cash handling with a pre-spend control platform built entirely on UPI infrastructure.

## **TL;DR**

- Most Indian companies still issue petty cash advances manually no spending limits, no real-time visibility, no easy reconciliation.

- CUPI replaces the cash envelope with a controlled UPI payout: the employee gets funds instantly, finance keeps full audit control.

- Approval workflows are configured before the payout happens, not chased after the fact.

- Every advance is tagged by purpose, capped by amount, and tracked by employee giving you audit-ready records without any manual data entry.

- Unspent funds can be reversed; receipts are captured at point of spend.

- CUPI integrates with accounting tools so reconciliation doesn't require a separate spreadsheet exercise.

- This isn't a reimbursement tool. It's pre-spend control which is a fundamentally different problem to solve.

## **Why Is Cash Advance Management Still Broken for Field Teams?**

Ask any Finance Head running a distributed sales or operations team and they'll describe the same situation: cash is handed to a field rep, a signed acknowledgment slip goes into a folder, and the next time finance thinks about it is when the rep submits a crumpled bundle of receipts three weeks later or doesn't submit them at all.

A route manager fills fuel worth ₹800 but submits a bill for ₹1,200. The difference is small enough that nobody questions it, but across 20 drivers and 30 days, the monthly leakage reaches lakhs.

This is not a field team problem. It's a system design problem. The controls that finance teams need approved amounts, spend categories, receipt capture, unspent balance recovery don't exist in a cash-based advance system.

The ACFE's 2024 Report to the Nations estimates that the typical organization loses 5% of its revenues each year to fraud, and more than half of cases were correlated with lack of internal controls or management override of internal controls.

Cash advances with no digital trail are exactly the kind of weak control that invites leakage often not through malice, but through ambiguity.

## **What Is Cash Advance Management?**

A **cash advance** is money issued to an employee _before_ they spend it, to cover anticipated business expenses. It's different from a reimbursement, where the employee spends their own money first and claims it back later.

**Cash advance management** is the set of controls around:

- Who can request an advance and for how much

- Who approves it and under what conditions

- How the money reaches the employee

- How spending is tracked against the advance

- How unspent funds are returned

- How the entire cycle is documented for audit

The problem with traditional cash advance management is that steps 3–6 above are almost entirely manual. Once physical cash leaves the company, control is gone.

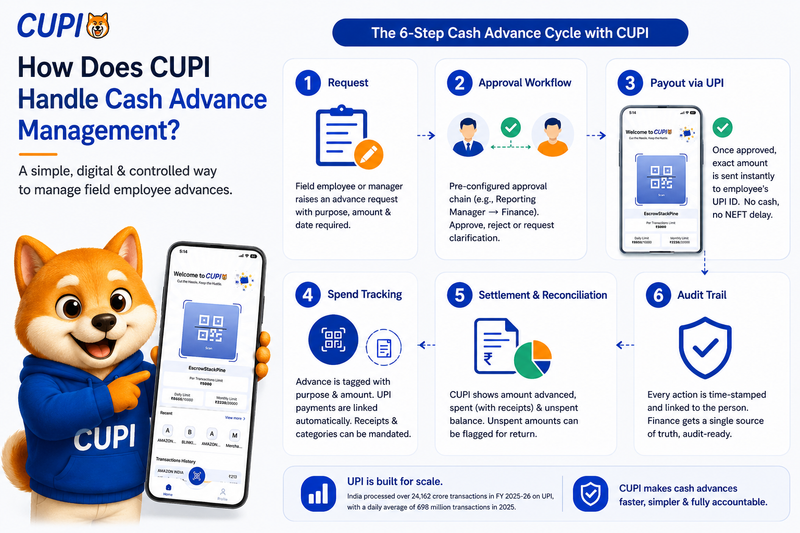

## **How Does CUPI Handle Cash Advance Management? (Step-by-Step)**

CUPI replaces the physical cash envelope with a controlled digital payout flow over UPI. Here's what a standard advance cycle looks like:

A simple visual guide to how CUPI manages field employee cash advances digitally using UPI, approval workflows, spend tracking, receipt matching, and audit-ready records.

**Step 1 — Request**

A field employee or their manager raises an advance request in CUPI, specifying: purpose (e.g., travel, client meeting, site materials), amount needed, and date required.

### **Step 2 — Approval Workflow**

The request goes through a pre-configured approval chain e.g., Reporting Manager → Finance. Each approver receives a notification and can approve, reject, or ask for clarification. No funds move without this step completing.

### **Step 3 — Payout via UPI**

Once approved, CUPI pushes the exact approved amount to the employee's registered UPI ID instantly, with no cash handling, no NEFT delay, no need for the employee to visit the office.

India processed over 24,162 crore transactions in FY 2025-26 on UPI, and UPI's daily average reached 698 million transactions in 2025 making UPI-based payouts a practical, universal delivery mechanism for field employees anywhere in India.

### **Step 4 — Spend Tracking**

The advance is tagged in CUPI with its purpose and amount. If the employee makes a UPI payment, the transaction is linked to the advance automatically. Spend categories and receipt uploads can be mandated before the next advance is issued.

### **Step 5 — Settlement and Reconciliation**

At the end of the cycle, CUPI shows: amount advanced, amount spent (with receipts), unspent balance. Unspent amounts can be flagged for return. The full record request, approval, payout, spend, receipt is exportable and accounting-tool ready.

### **Step 6 — Audit Trail**

Every action in the cycle is time-stamped and linked to the person who took it. Finance has a single source of truth instead of a folder of paper slips.

## **What Controls Do Finance Teams Actually Care About?**

Finance Heads and CFOs running field teams consistently need the same five controls. Here's how each one maps to the CUPI workflow:

### **Spend Limits Per Employee**

Set a maximum advance amount per employee, per trip, or per month. An advance request above the limit is automatically flagged or blocked the approver sees a clear reason.

### **Purpose-Based Approvals**

An advance tagged "client meeting" follows a different approval path than one tagged "equipment purchase." CUPI lets you configure workflows by category, not just by amount.

### **No-Receipt, No-Next-Advance Rule**

Finance can enforce a policy where a new advance is blocked until receipts for the previous one are uploaded and reconciled. This addresses the most common gap in cash-based systems: receipts submitted weeks late, or not at all.

### **Unspent Balance Recovery**

When an employee spends ₹1,200 of a ₹2,000 advance, the ₹800 balance should return to the company account not stay in the employee's personal account indefinitely. CUPI tracks this balance and flags it for reversal.

### **GST and Cost Centre Tagging**

Every advance can be tagged to a cost centre, project code, or client so P&L owners and finance can see field spending by business unit without a separate spreadsheet exercise. GST-compliant receipt capture is supported where applicable.

## **Real Use Cases: Who Actually Uses This?**

### **Use Case 1 — Field Sales Team, FMCG Distributor (150 Reps)**

A regional FMCG company's field reps needed daily cash for beat expenses: travel, market activation, and small vendor payments. Previously, cash was handed out at weekly branch meetings. With CUPI, reps receive approved daily advances over UPI by 8 AM. Managers approve from mobile. Finance reconciles weekly instead of monthly.

### **Use Case 2 — Site Supervisors, Infrastructure Company**

Site supervisors handle petty cash for labour payments and material purchases at remote locations. Physical cash handling was a security risk. CUPI advances to their UPI ID, capped per day, with mandatory receipt upload before the next day's advance is released.

### **Use Case 3 — Service Engineers, Electronics Company**

Service engineers travel to customer sites across Tier 2 and Tier 3 cities. Advances for travel and spare parts were previously reimbursed 30–45 days after the trip. CUPI shifted this to a pre-approved advance model: engineers receive funds before travel, finance closes the books within 7 days of trip completion.

### **Use Case 4 — Inside Sales + Field Ops, B2B SaaS Company**

An ops team needed advance management for field visits to onboard SME clients. The advance amounts were small (₹500–₹2,000 per visit), but volume was high (200+ visits/month). Manual processing was creating accounting backlogs. CUPI automated approvals below ₹1,000 and routed larger amounts to the Finance Head.

### **Use Case 5 — Distributor Payment Operations**

A company making payments to small distributors and channel partners used informal cash advances as bridge funding. CUPI allowed them to formalize the process: defined limits per partner, approval by the Sales Head, payout via UPI, settlement against invoices.

### **Use Case 6 — Multi-city Events and Activations Team**

A marketing team running BTL activations across 12 cities needed petty cash for local vendor payments. Central finance couldn't manage 12 different city coordinators individually. CUPI gave each city coordinator a separate wallet with a defined budget, with the Finance team approving top-ups centrally.

## **Comparison: CUPI vs Cash vs Reimbursements vs Cards vs Bank Transfers**

**Criterion**

**Physical Cash**

**Reimbursement**

**Corporate Card**

**Bank Transfer (NEFT/IMPS)**

**CUPI (UPI-based)**

**Speed of funds to employee**

Instant (if in-office)

15–45 days after spend

Instant (if issued)

Same-day to next-day

**Instant via UPI**

**Pre-spend approval**

Informal / none

After-the-fact

Partial (spend limits)

Manual, case-by-case

**Structured approval before payout**

**Spending control**

None after handover

None (already spent)

Category blocks possible

None after transfer

**Per-advance limits + purpose tags**

**Receipt capture**

Paper, manual

Email/PDF submission

Card statement only

None

**Mandatory digital capture, in-flow**

**Audit trail**

Paper slips / none

Expense reports

Bank statements

Bank records

**Full digital trail: request → approve → pay → spend → settle**

**Unspent balance recovery**

Informal / delayed

N/A

Carry-forward or block

No automatic mechanism

**Tracked + flagged for reversal**

**GST / cost centre tagging**

Manual

Manual, error-prone

Possible, partial

None

**In-workflow tagging**

**Accounting integration**

Manual entry

Manual or CSV

Partial auto-sync

Manual reconciliation

**Export-ready / integration-ready**

**Scalability (50+ field reps)**

Very difficult

Operationally heavy

High card issuance cost

High ops overhead

**Scales without additional headcount**

**Works in Tier 2/3 cities**

Yes

Yes

Limited POS coverage

Yes

**Yes — UPI is near-universal**

## **Conclusion: Pre-Spend Control Is the Only Kind That Works**

Cash advance management is a solved problem in theory. In practice, most Indian companies are still operating with a system that was designed for a world without UPI, without mobile approvals, and without the expectation that finance should have real-time visibility into field spending.

The issues aren't unusual or extreme. A field rep receiving an advance and spending it without structured tracking is entirely normal. What's changed is that the tools to do this differently now exist and they work on infrastructure (UPI) that's already in every employee's phone.

CUPI doesn't claim to eliminate all expense fraud or guarantee specific savings figures. What it does is replace an opaque, manual process with a traceable, controllable one. That's what finance teams have been asking for.

Stop reconciling cash advances at month-end. CUPI gives your field team instant UPI payouts and gives finance real-time control from request to settlement. → _Get started with CUPI, talk to the team today_

# FAQs

Q: What happens if an employee spends less than the advance amount?

A: The unspent balance is tracked in CUPI against that specific advance. Finance can flag it for reversal and the employee can return funds via UPI to the company account. The settlement is recorded against the original advance for a clean close.

Q: Does CUPI integrate with Tally or other accounting tools?

A: CUPI is designed to export reconciled advance data in formats compatible with standard accounting workflows. Check with the CUPI team for the current integration list, as these are updated regularly.

Q: How does the approval workflow work if a manager is traveling?

A: Approvals in CUPI are mobile-accessible. Managers can approve, reject, or query advances from any device. Escalation paths can be configured so that if the primary approver is unavailable for a defined period, the advance routes to a secondary approver automatically.

Q: Is there a minimum or maximum advance amount?

A: CUPI doesn't enforce a platform-level minimum or maximum. Your finance team configures the limits appropriate to your policy by role, category, or total outstanding advance per employee.

Q: Can we run CUPI for contract staff or third-party agents, not just full-time employees?

A: This depends on your onboarding and KYC configuration. Speak with the CUPI team about how third-party payees can be added to your advance workflows. The core platform supports multiple payee types, subject to your internal policy.

Q: Is CUPI a prepaid card or a wallet?

A: CUPI is neither. It's a controlled payout platform that pushes approved funds directly to an employee's existing UPI ID. The employee doesn't need a new card or a separate app wallet they receive money to the UPI address they already use.

Q: Can we set different advance limits for different employee grades?

A: Yes. CUPI lets you configure advance policies by role, team, or individual so a junior field rep might have a ₹1,500 daily limit while a senior territory manager gets ₹5,000, with different approval chains for each.

Q: How does CUPI handle receipt submission?

A: Employees upload receipts directly in CUPI photo of the bill, linked to the specific advance and spend transaction. Finance can enforce a policy where no new advance is issued until the prior advance's receipts are submitted.

Q: What if a field employee doesn't have a smartphone?

A: UPI requires a smartphone, but over 500 million people use UPI in India, and penetration is deep into Tier 2 and Tier 3 markets. For employees without smartphones, operational leads or team managers can receive advances on their behalf and manage disbursement locally CUPI tracks the advance at the responsible person level.

Q: How is this different from just doing a bank transfer to the employee?

A: A bank transfer gets money to the employee but creates zero control or trackability at the purpose or category level. With a direct transfer, finance has no visibility into what the money was spent on, no receipt capture mechanism, and no way to flag an unrecovered balance until someone reconciles manually, often weeks later. CUPI wraps the transfer in a structured workflow.

---

This blog is powered by Superblog. Visit https://superblog.ai to know more.

---

## How to Track Cash Advances in a Company

Author: Nithish B

Author URL: https://blog.getcupi.com/author/nithish-b

Published: 2026-06-01

Category: Writing

Category URL: https://blog.getcupi.com/category/writing

Meta Title: How to Track Cash Advances in a Company | CUPI

Meta Description: Learn how finance teams track, control, and reconcile cash advances — with approval workflows, UPI-native payouts, and real-time audit trails using CUPI

URL: https://blog.getcupi.com/blog/how-to-track-cash-advances-in-a-company

### Learn how finance teams track, control, and reconcile cash advances with approval workflows, UPI-native payouts, and real-time audit trails using CUPI

A practical guide for finance teams to manage requests, approvals, payouts, and reconciliations with complete visibility and control.

**How to Track Cash Advances in a Company (A Finance Team's Practical Guide)**

## TL;DR

- A cash advance is company money given to an employee _before_ a business expense occurs - unlike reimbursements, which happen after.

- Most companies lose track of advances because there's no structured approval, no spend limit, and no automated reconciliation - just trust and follow-up emails.

- The right tracking system creates a four-step chain:

**request → approval → controlled payout → reconciliation**.

With CUPI, UPI rails compress this into near real-time - eliminating the manual request-and-wait bottleneck entirely.

- With CUPI, the employee operates as an authorized user within the company's corporate account - spend-capped and purpose-locked - not as an independent recipient of a personal payout.

- Cash advances without controls create three specific risks: float abuse (money sits with employees too long), category drift (spends go outside approved purpose), and duplicate or inflated claims.

- Key controls finance heads should require: per-advance spend caps, purpose tagging, receipt mandates, and a hard settlement deadline.

- A structured system doesn't just prevent fraud - it cuts month-end close time because reconciliation is already done by the time you need it.

Key Takeaways

Definition - A cash advance in a business is money issued to an employee before a business expense occurs. Unlike reimbursements — where the employee pays first and claims back later — a cash advance puts company money out first, with the employee accountable for spending it correctly and settling with receipts.

[See How CUPI Works](https://www.getcupi.com/) [Book a Demo](https://kyc.getcupi.com/basic-kyc)

## **What Is a Cash Advance — and Why Is It Hard to Track?**

A **cash advance** is money your company gives an employee _ahead of_ an expense. The employee spends it, then accounts for it. This is different from a reimbursement (where the employee pays first, claims later) and different from a corporate card (where the company pays a bank bill after the fact).

Cash advances show up across most operations-heavy Indian businesses:

- A sales rep travelling to a Tier-2 city for a client visit

- A field executive who needs to pay a local contractor in cash

- A procurement officer picking up supplies from a vendor who doesn't accept NEFT/cards

- A logistics coordinator managing last-mile expenses across multiple routes

The reason tracking breaks down is structural. Most businesses issue advances informally a message, a transfer, and a reminder to "submit bills by Friday." There's no system enforcing that. The result is open float (advances that haven't been settled), no audit trail, and reconciliation that depends on people chasing people.

## **Why Does This Matter to Finance Teams Right Now?**

According to the RBI's Payment Systems Report, UPI accounted for 85.5% of digital payment transaction volume in H2 2025 yet most internal employee payout workflows haven't caught up. Companies run UPI for everything external, but internally, cash advances still flow through informal bank transfers with zero controls attached.

UPI recorded 228.3 billion transactions in 2025, up from 172.2 billion in 2024 a 29.3% volume increase. Every operations-heavy company is touching UPI daily. The infrastructure exists. The controls layer on top of it often doesn't.

The practical consequence: finance teams spend time they don't have chasing settlement on money they've already sent out.

## **How Does a Cash Advance Tracking System Work? (Step-by-Step)**

A structured cash advance workflow has four stages. Here's what each one should look like in practice.

A simple blog visual explaining how CUPI helps companies track cash advances through requests, approvals, UPI-based payouts, receipt matching, and real-time reconciliation.

### **Step 1 — Request**

In a traditional system, the employee submits a request specifying:

- Amount needed

- Purpose (travel, procurement, field ops, etc.)

- Date of expense

- Expected settlement date

This creates a paper trail from moment zero no more verbal approvals. But this step is also where most processes stall. Requests wait in inboxes. Approvals lag. Employees follow up. Money eventually moves, but the expense has often already happened by then.

**With CUPI, this bottleneck doesn't exist.** Because CUPI operates on UPI rails, spend data is captured at the point of transaction in near real-time against a pre-configured corporate account. The company's guardrails (spend caps, purpose categories, MCC restrictions) are already set at the account level. There's no slow request-and-wait cycle before an employee can operate. The controls travel with the account, not the approval email.

### **Step 2 — Approval**

A configurable approval chain reviews and approves (or rejects) the request. In CUPI, this is multi-level a team lead approves, then a finance manager, depending on the amount bracket. Approvals happen on mobile, so the process doesn't wait for someone to be at a desk.

Critical controls at this stage:

- Spend cap enforcement (you set ₹5,000 max for this category; the system won't let you approve ₹12,000 without an override)

- Purpose-category locking (a "travel" advance can't be used for procurement)

- Validity window (the advance is active for 3 days; unused amounts auto-expire)

### **Step 3 — Controlled Payout**

Once approved, the advance is activated within the company's corporate account on UPI rails. The employee isn't receiving a personal payout into their own account they're operating as an authorized user within the company's account, with a pre-defined spend envelope attached to their role or trip.

The company remains the account holder throughout. The employee operates within guardrails set by finance: spend cap, purpose category, MCC restrictions, and validity window. They can transact at any UPI QR kirana, fuel pump, logistics vendor without needing a card or physical cash. But every rupee spent is debited from the corporate account, not a personal float.

Every transaction is logged in real time against the advance ID.

### **Step 4 — Reconciliation**

After the expense window closes, the employee submits receipts. CUPI matches spend data (already captured from the UPI transaction) against submitted bills. Unmatched or over-limit spends flag automatically. Settled amounts close the advance; unspent amounts are flagged for return.

Finance doesn't chase anyone. The data is already there.

## **What Controls Do Finance Teams Actually Need?**

Most finance heads don't need more data they need fewer exceptions. These are the controls that eliminate the common failure points:

### **Per-Advance Spend Caps**

Every advance should have a hard ceiling. ₹2,000 for local field ops. ₹15,000 for outstation travel. The system enforces these it doesn't just recommend them.

### **Purpose Tagging**

An advance issued for "client visit Chennai" should not be reconcilable against grocery receipts. Purpose tagging lets finance categorise spend at issuance and flag deviations at reconciliation.

### **Settlement Deadlines with Auto-Escalation**

The advance closes on Day 5. If the employee hasn't submitted receipts, the system escalates first a reminder, then an alert to their manager. No manual follow-up required.

### **Merchant Category Restrictions (MCCs)**

For companies using CUPI's UPI payout layer, you can restrict which merchant categories an advance can be used at. A logistics advance can include fuel (MCC: 5541) and toll (MCC: 7523). It cannot include restaurant charges (MCC: 5812) unless approved separately.

### **Immutable Audit Trail**

Every action — request, approval, payout, spend, receipt upload, settlement is timestamped and stored. This is what your auditor needs. This is what prevents disputes.

### **Configurable Approval Chains**

Not every advance needs the CFO's sign-off. A ₹1,500 petty cash advance should clear in one step. A ₹50,000 vendor payment advance might need three. Configure by amount bracket, not by individual exception.

## **Real Use Cases: How Companies Track Advances in Practice**

### **Use Case 1 — Field Sales Team (50+ reps, Tier-2/3 cities)**

A FMCG distributor has 60 sales reps operating across Karnataka and Tamil Nadu. Previously, advances were issued via informal IMPS transfers. Settlement was weekly except when it wasn't. With CUPI, each rep is set up as an authorized user within the company's corporate account, with a trip-scoped spend limit pre-configured by finance. Spend is captured automatically at point of transaction. Finance reconciles 60 accounts in an afternoon instead of three days.

### **Use Case 2 — Procurement Ops (Local Vendor Payments)**

A manufacturing SME needs to pay local raw material suppliers who don't accept NEFT but do accept UPI QR. The procurement officer gets a purpose-locked advance of ₹40,000 for approved vendor categories. Every payment scans directly at the vendor's QR. Receipt and transaction data are already matched by the time the bill is submitted.

### **Use Case 3 — Event / Marketing Ops**

A marketing team running a product launch needs ₹1.2L in operational cash venue deposits, logistics, F&B for a 2-day event. Instead of one large transfer with zero visibility, CUPI issues category-split advances: ₹40k venue, ₹30k logistics, ₹25k catering, ₹25k contingency. Each category reconciles separately. Post-event close takes 2 hours, not 2 weeks.

### **Use Case 4 — Site Ops / Construction**

A mid-size construction company runs 12 active sites. Each site supervisor needs daily petty cash for materials, labour, and sundries. CUPI issues daily rolling advances with auto-reset. Supervisors spend via UPI. Finance gets a consolidated site-wise spend dashboard in real time.

### **Use Case 5 — Logistics / Fleet Management**

A logistics company with 200 drivers issues per-trip advances for fuel, toll, and maintenance. With MCC restrictions, fuel-only advances can't be used at restaurants. GPS tagging on select spends confirms location at point of spend. Month-end close is pre-reconciled.

### **Use Case 6 — RevOps / Client Onboarding Costs**

A SaaS company's customer success team incurs onboarding-related costs travel, software subscriptions, small vendor payments. These used to flow through personal cards and reimbursement claims. With structured advances, CSM spend is tagged to the client account from day one. Finance and RevOps have shared visibility into cost-per-account.

## **Comparison Table: CUPI vs Cash vs Reimbursements vs Cards vs Bank Transfers**

**Feature**

**CUPI (UPI Advances)**

**Cash**

**Reimbursements**

**Corporate Cards**

**Bank Transfers (IMPS/NEFT)**

Pre-approval workflow

✅ Configurable, multi-level

❌ Usually verbal

✅ Post-spend approval

✅ Card issuance approval

❌ Typically none

Spend controls

✅ Amount + MCC + purpose

❌ None

❌ After spend occurs

⚠️ Partial (card limits)

❌ None

Real-time visibility

✅ Per transaction

❌ Not until submitted

❌ Not until claimed

✅ Statement-level

⚠️ Transfer visible; spend invisible

Audit trail

✅ Immutable, timestamped

❌ Depends on receipts

⚠️ Claim records only

⚠️ Bank statements

⚠️ Transfer record only

Reconciliation effort

✅ Low — auto-matched

❌ High — manual

❌ High — manual claims

⚠️ Medium

❌ High

UPI acceptance (India)

✅ 55M+ QR codes

❌ N/A

❌ N/A

❌ Low (7.8M POS terminals)

❌ Not usable at merchant

Settlement tracking

✅ Deadline + auto-escalation

❌ Manual follow-up

❌ Manual follow-up

❌ Statement-dependent

❌ Manual

Suitable for field ops

✅ Yes

✅ Yes (no controls)

❌ Requires personal cash

❌ Low acceptance in Tier-2/3

❌ Not at-point-of-spend

Risk of leakage

🟢 Low

🔴 High

🟡 Medium

🟡 Medium

🔴 High

Setup speed

✅ Fast (digital KYC)

✅ Instant

❌ Process-dependent

❌ 10–15 days typical

✅ Fast

## **Conclusion**

Tracking cash advances isn't a complex problem. It's a process problem the work is done manually because most companies never built the system to do it automatically.

The switch to structured advance management doesn't require a large implementation. It requires four things: a request step, an approval chain, a controlled payout, and a reconciliation close. A modern system handles all four without the delays that make the traditional process frustrating.

If your finance team is still chasing settlement emails at month-end, that's the clearest sign the current process isn't scaling.

# FAQs

Q: Q1. What is a cash advance in a business context?

A: A cash advance is company money issued to an employee before a business expense occurs. The employee spends it for an approved purpose — travel, procurement, field ops — and then settles by submitting receipts. It's different from a reimbursement, where the employee pays first and claims back later.

Q: Q2. How do companies typically track cash advances?

A: Most companies track advances through a combination of spreadsheets, email approvals, and manual receipt collection. This works at low volume but breaks down quickly as headcount or field operations grow. The core problem: there's no control on how the money is spent after it leaves the company account.

Q: Q3. What's the difference between a cash advance and petty cash?

A: Petty cash is a fixed float maintained at a location (office, site, branch) for small incidental expenses. A cash advance is issued to a specific employee for a specific purpose and expected to be settled individually. Petty cash is replenished in bulk; cash advances are tracked and settled per person.

Q: Q4. What happens if an employee doesn't settle a cash advance?

A: Without a formal system, nothing — until someone follows up manually. With CUPI, the advance has a hard settlement deadline. If the employee doesn't submit receipts by the deadline, the system auto-escalates to their manager. Repeat non-settlement can flag the employee for policy review.

Q: Q5. Can cash advances be issued via UPI in India?

A: Yes. CUPI issues advances via UPI directly to employee accounts or wallets. This means the employee can spend at any UPI-accepting merchant — the same 55M+ QR codes your customers use. It eliminates the "card didn't work" problem that forces staff back to physical cash in Tier-2/3 markets.

Q: Q6. What controls can a finance team put on a cash advance?

A: The most important controls are: (a) a spend cap, (b) a purpose category that limits what the advance can be used for, (c) a settlement deadline, and (d) a required receipt upload. CUPI enforces all four programmatically — not as policy suggestions, but as system constraints.

Q: Q7. How does cash advance reconciliation work?

A: In a structured system, reconciliation matches three things: the approved amount, the actual spend (captured at transaction level), and the submitted receipts. CUPI auto-matches UPI transaction data against submitted bills. Discrepancies flag automatically. The finance team reviews exceptions — not every line item.

Q: Q8. What's the biggest risk with untracked cash advances?

A: Float abuse — money sitting with employees beyond the expense window. The secondary risk is category drift: a travel advance used for non-travel spend. Both are invisible without a spend-control layer. Audit exposure is significant: advances without proper documentation create unexplained outflows that auditors will question.

Q: Q9. Do I need a cash advance policy before implementing a tool?

A: Ideally, yes — the policy sets the rules the system enforces. At minimum, you need: advance categories, spend caps per category, settlement timelines, and the approval chain per amount bracket. CUPI can be configured around an existing policy or help you structure one from scratch during onboarding.

Q: Q10. How is CUPI different from a corporate card program?

A: Corporate cards are payment instruments — they allow spend but don't enforce purpose or reconcile automatically. CUPI is a controls platform: every payout is pre-approved, purpose-tagged, spend-capped, and reconciled against receipts. Cards also take 10–15 days to issue physically; CUPI can go live via digital KYC in under 24 hours.

---

This blog is powered by Superblog. Visit https://superblog.ai to know more.

---

## Sample Page

Author: Nithish B

Author URL: https://blog.getcupi.com/author/nithish-b

Published: 2026-06-01

URL: https://blog.getcupi.com/sample-page

This is a page. Notice how there are no elements like author, date, social sharing icons?

Yes, this is the page format. You can create a whole website using Superblog if you wish to do so!

---

This blog is powered by Superblog. Visit https://superblog.ai to know more.

---